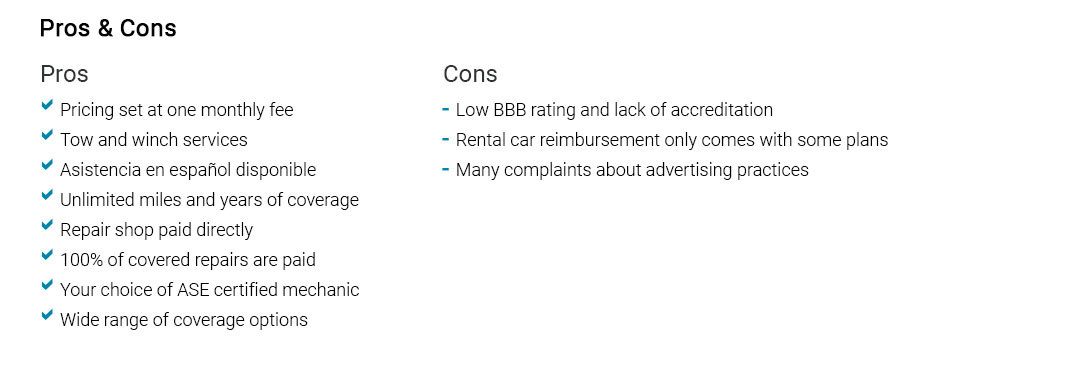

|

|

|

|

|

|

|

|

|

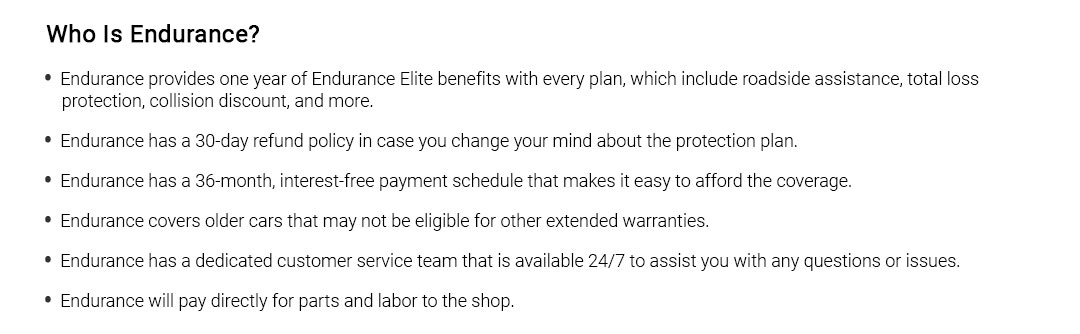

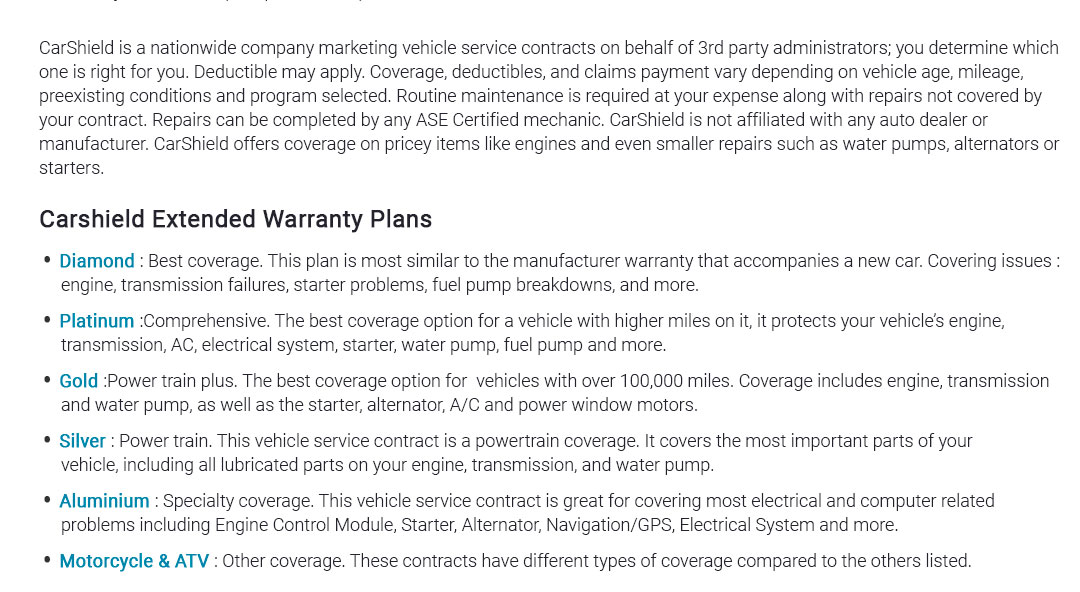

|||

|

|

|

|||||||

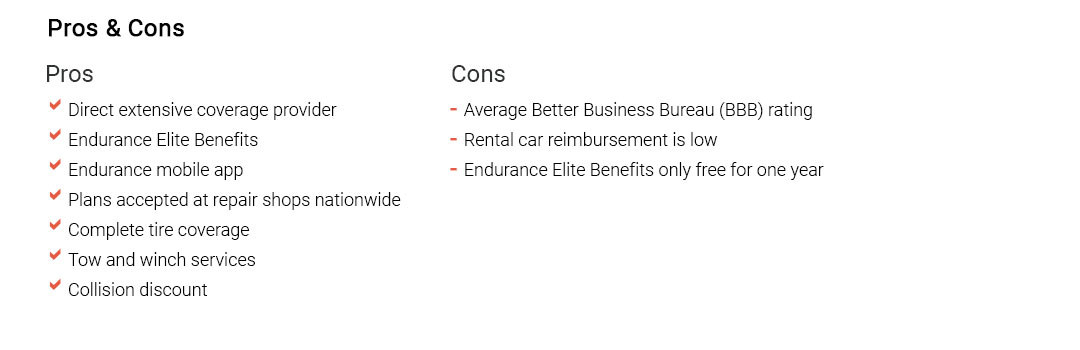

|

|||||||

|

|||||||

|

|||||||

|

|||||||

|

|||||||

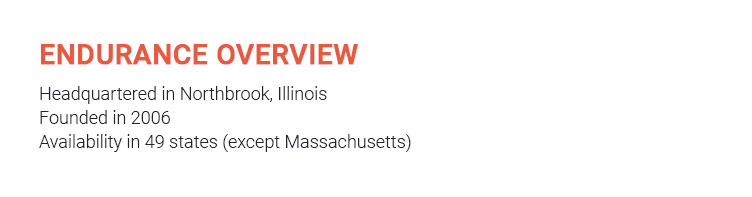

|

||||||

|

||||||

|

||||||

|

||||||

|

|

|

|

|

|

|

|

classic gap insurance explained with practical tips for careful driversWhat it isGap insurance fills the difference between what your auto policy pays after a total loss and the higher figure you still owe or the price you originally paid. With classic gap insurance, the focus is on vehicles that hold sentimental value, have limited production, or sit in the early stages of restoration and financing. The goal is simple: avoid writing a big check after bad luck. How it works in practiceOn a wet Thursday, a client called after his 1994 coupe was rear-ended and declared a total loss. The comprehensive carrier offered an actual cash value that trailed his remaining loan and recent upgrade receipts. His classic gap policy filled a £9,800 shortfall, turning a stressful week into a manageable one. No windfall, just closure. Who benefits most

Common types you'll encounter

What it usually doesn't do

Calculating your gap

Quick rule-of-thumbIf the projected shortfall exceeds three months of your take-home pay, classic gap insurance is worth a serious look. Soft disagreement, fairly putSome enthusiasts argue a strong emergency fund and an agreed value policy make gap unnecessary. That can be true for well-capitalized owners with dialed-in coverage. I've found, though, that documentation gaps, timing quirks, and lender rules still leave room for unpleasant surprises that gap neatly resolves. Buying and using tips

Claims flow you can expect

Documentation checklist (small but mighty)

Costs and valuePremiums vary with loan size, car rarity, and claim history. The value is clearest during the first 24 - 36 months after purchase or major work, when depreciation and financing balance create the widest gap. Final guidanceUse classic gap insurance as a precision tool: pick the type that fits your base policy, calibrate the limit to your true exposure, and keep your paperwork tight. Peace of mind comes from the fit - not from the label on the policy. https://www.classictrak.com/products-and-programs-2/

As with many of our Classic GAP programs, GAP Care is available in most states, covers vehicles up to 14 model years prior, and offers up to $1,000 deductible ... https://www.classictrak.com/products-and-programs_classic/

As with many of our Classic GAP programs, GAP Care is available in most states, covers vehicles up to 14 model years prior, and offers up to $1,000 deductible ... https://dashboard.classictrak.com/consumer/

At this time Classic GAP and Theft claims are processed through this portal. For all other products, please review your contract for claim processing ...

|